6 in 10 Americans have a retirement account, while only 1 in 3 have an estate plan.

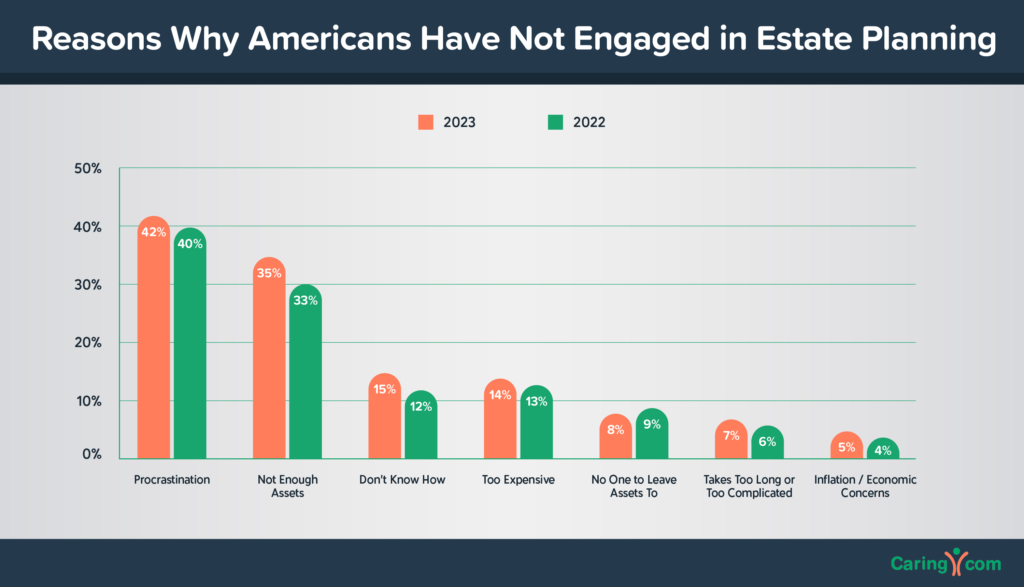

While the majority of Americans see the importance of retirement planning, most neglect estate planning. The most common reason for avoiding a will, trust or estate plan? Procrastination.

Todd Stanley, a wheat and corn grower from Grygla, Minnesota, recently worked with Pinion to update his existing estate plans.

“For years I put off updating our estate plan because it was never the right time. But I realized it would always be that way – something would always get in the way until it was urgent or too late. But you can’t run the world from the grave, you have to take care of things while you can.”

What this Means for Your Legacy

It doesn’t matter what the reason is – as long as you realize that by choosing not to plan, you are actually saying you are ok with these three major repercussions (one of which is highly time-sensitive):

-

Your assets will go through public probate.

Without a proper estate plan, a probate court will most likely determine what happens to your assets. Settling estates this way can be a lengthy, costly, and emotionally draining process, as it unfolds in the public eye and often leaves the family with limited control.

The average probate process costs 5% to 10% of an estate in legal fees and administrative costs, with some estates losing 20%. Other fees include court fees, a probate bond and executor compensation.

An estate plan ensures your assets, land, investments and retirement accounts, all land in the right hands without a lengthy, public, and expensive probate. This is the best way to protect your family, your legacy and your life’s work.

-

Your beneficiaries will pay more in taxes.

Creating an estate plan now – with the current provisions – could save your beneficiaries from a hefty tax bill. You may feel like you’re saving money by not investing in an estate plan now, but it could be the difference between your entire estate going to your family and nearly half of it being taxed away.

The government can currently tax up to 40% of an estate over $12.92 million ($13.61 million in 2024). However, things are set to change at the end of 2025. Unless the administration / Congress extends the current provisions – the government will be able to tax up to 40% of any estate over $7 million.

What this might look like:

|

|

Current Law |

Proposed Changes for 2026 |

|

Exemption (Individual) |

$12.92 M (2023); $13.61 M (2024) |

$7 M* |

|

Exemption (Married) |

$25.84 M (2023); $27.22 M (2024) |

$14 M* |

|

Estate and Gift Tax Rate |

40% |

40% |

*Estimated

“Until we know the outcome of the 2024 election and what may be passed by Congress, planning remains a challenge,” says Jim Rein, who leads the Next Gen functional area for Pinion.

“However, those who prepare for multiple scenarios and outcomes are always better positioned to pivot and adjust for the greatest benefits.”

-

Your loved ones will wrestle over major decisions.

Money, business, and land are all deeply personal. Leaving important decisions to grieving family with differing opinions and desires, is a recipe for strife. An estate plan minimizes room for conflict, making it easier to process together rather than against each other.

Rein describes a common scenario he comes across too often – a business owner procrastinated in establishing an estate plan for his farm and he passed away unexpectedly.

During a Midwest family operation tour, a Pinion client noted a neighboring property’s decline. A decade before, it had thrived with excellent management and well-maintained equipment. Sadly, after the patriarch’s passing, the surviving family fought over the estate for years and the operation fell into disarray.

Don’t wait until it’s an emergency

Most people wait for a medical diagnosis or another triggering event to start the estate planning process. However, this often too late as it can take several months or up to a year to prepare and implement an estate plan. An emergency is not the time to take action.

Too often, lack of planning creates a tax bill that heirs can’t afford without selling part or all of the estate…. which is often a family-owned business. So don’t kick the can down the road.

“Give yourself and your loved ones the peace of mind knowing your business, wealth and legacy are in good hands,” says Rein.

“Don’t pass the buck onto someone else – especially not to Uncle Sam.”

To evaluate your estate tax plan, maximize your returns, or position yourself for tax law benefits ahead of changes, contact a Next Gen Pinion advisor.