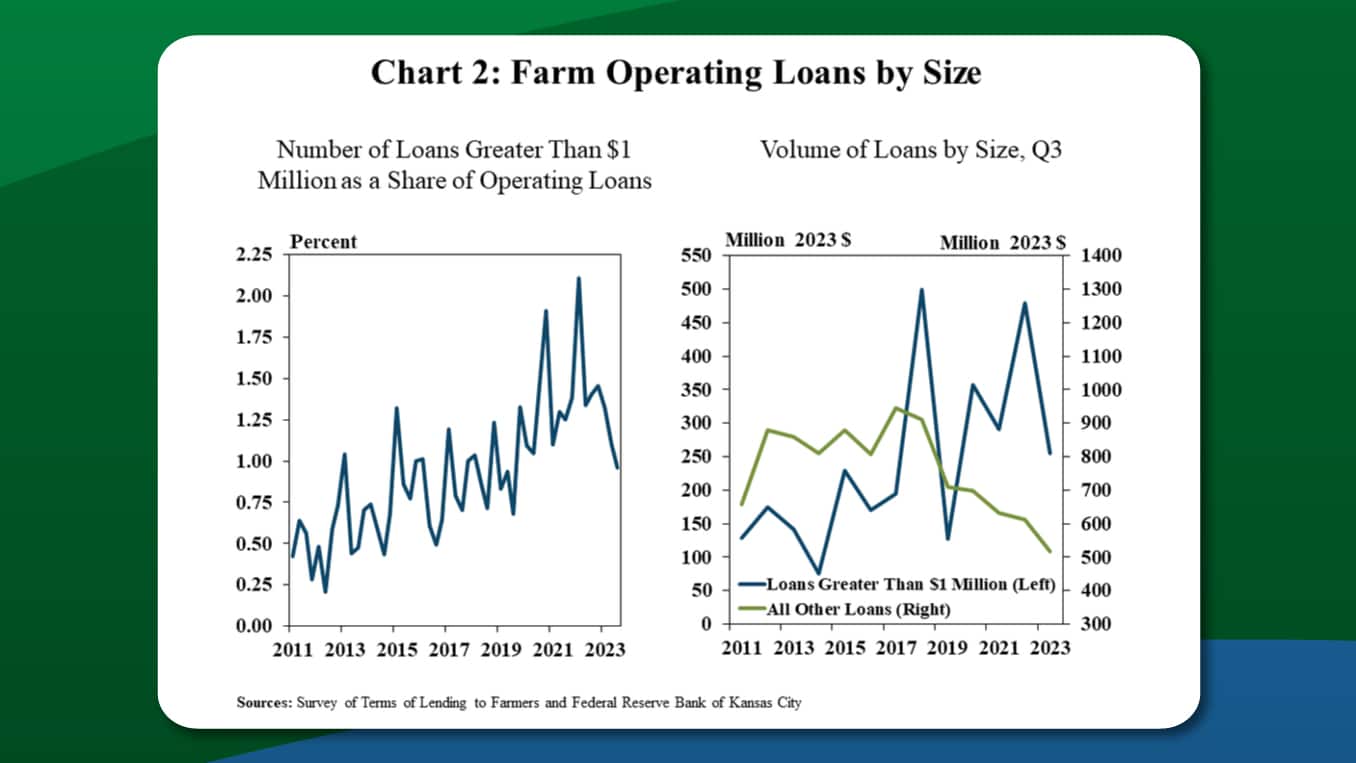

After nearly two years of rising interest rates, many farmers are tapping into their cash reserves from prosperous years to avoid taking out new loans. The Federal Reserve Bank of Kansas City reports that lending has softened with the amount of farm operating loans over $1 million dropping notably and the reduction in loan size contributing to the third consecutive quarter of declines in non-real estate farm loan volumes.

Many farmers are leaning on their cash reserves to limit their debt usage. However, as commodity prices have dropped and input costs rise, farmers are feeling the pinch of thinner profit margins. While they may have a large cash reserve built up from prosperous years, their credit needs are also increasing.

This creates a dilemma – should you use your cash reserves to pay down existing debt, or do you hang onto those loans and your liquidity to cash flow future expenses and avoid the record high interest rates? The average interest rate on various types of farm loans, after rising for nearly two years, has reached the highest level since 2007, standing at 8.34%. And this isn’t expected to decline in 2024.

“While paying down debt is typically a wise financial goal, it may cost you more to deplete your excess cash if you have to turn around in 2024 and get caught in the higher rate environment,” says Pinion business advisor Derrick Deardorff. “Each operation is different, but this may not be the year to aggressively attack your farm loans.”

Instead, Pinion advisors share their tips for avoiding this cycle, building cash reserves, and navigating the high interest rates in 2024.

5 Steps to Navigate High Interest Rates in 2024

1. Conduct a cash flow analysis. Get familiar with how much is coming in each month, vs. what is going out. Understand exactly how much working capital you need to operate month to month – this will tell you what you need stocked up in your war chest to survive the downtimes. Make sure you take advantage of short-term investments and money market accounts to put your excess cash to work until needed.

2. Plan two to four years out. Before making any major moves to reduce debt structure, make sure you are set up with enough working capital to navigate two to four years ahead if commodity prices stay down. What equipment will need to be replaced? What investments will you need to make in that time? Estimate what it will require to operate over the next few years and work to conserve it.

“If worst case scenario is needing $10 million to make it through the next three years, make sure to conserve that, versus using the working capital to pay off debt, machinery or other ag loans,” says Deardorff.

3. Know your cost of carry. Work on your risk management and grain marketing plan and understand what it would cost to carry grain to market at a later date. For instance, if you’re holding out for higher grain prices – you need to ensure that you’ll be able to sell that grain for a price that justifies the interest rate you’re paying or could be earning on that inventory converted to cash in the meantime.

[Sign up for daily grain market reports]

4. Explore all lending options. When it comes down to it and you need to take out a loan, shop around for the best rates and options. You may have a strong relationship with a lender, but they may not be getting you the best rate on the market. Explore alternative lending options, negotiate the terms and conditions, and ensure you have liability protection.

5. Avoid recency bias. “One of the biggest pitfalls I’ve seen is farmers falling into recency bias,” says Deardorff. “Coming off a great two years and into a dramatically different environment where margins from those strong years are not carrying forward could be a rude awakening.”

As you navigate the new year, understand your numbers, run the forward projections, and build a strong team to help you make data driven decisions. Communicate early and well with your lender, accountant, farm business management advisor, and all the folks on your team.

“The silver lining is that most producers are sitting on a bit of cash and we’re seeing the FEDs pause rate hikes,” says Deardorff. “It’ll be important to shore up your cash reserves and weather through these peak rates until the lending environment shifts.”

Pinion ag advisors provide producers with marketing and risk management services designed to increase profitability and reduce volatility. Connect with an advisor for guidance on navigating the fast-moving markets and high interest rates in 2024.